The global real estate landscape has experienced a profound recalibration in the post-pandemic era, with international capital increasingly pivoting toward the Asia-Pacific (APAC) region as investors reset their portfolios for the next phase of the economic cycle. Within this macro-regional shift, the Indonesian archipelago and specifically the island of Bali has emerged not merely as a speculative frontier, but as a maturing, institutional-grade asset class. As the market enters 2026, the era of uncalculated, hype-driven property development has largely concluded. The modern property investment Bali ecosystem is currently defined by a flight to operational quality, strict regulatory compliance, and a strategic alignment with multi-billion-dollar infrastructure initiatives that are physically reshaping the island’s economic geography.

For institutional allocators, family offices, and sophisticated private investors seeking to deploy capital within the top real estate districts Bali has to offer, reliance on anecdotal evidence is no longer viable. Success in 2026 requires a rigorous, data-driven methodology. By synthesizing official Bali BPS property data (Badan Pusat Statistik), Bank Indonesia macroeconomic indicators, and proprietary market intelligence from Tier 1 global property consultancies including Knight Frank, Colliers International, and JLL this report provides an exhaustive analysis of the island’s property sector. It dissects the historical growth metrics that have defined the past decade, identifies the five most profitable districts for current capital deployment, and projects the long-term impact of transformative infrastructure on future land valuations.

Bali Real Estate Market Analysis: Historical Growth (2016-2026)

To contextualize the stabilization and subsequent institutionalization of the Bali property market in 2026, it is imperative to conduct a granular examination of the market’s historical volatility and growth arc. The trajectory of Bali real estate statistics over the past decade can be segmented into three distinct economic phases: the pre-pandemic acceleration (2016-2019), the systemic pandemic shock and ensuing highly speculative recovery (2020-2025), and the current phase of structural recalibration and market maturity (2026).

The fundamental engine driving Bali’s Gross Regional Domestic Product (GRDP) and its corresponding real estate valuations has perpetually been international and domestic tourism. Prior to the global pandemic, Bali experienced a sustained, robust expansion in visitor volumes. Official data from Statistics Indonesia (BPS) Bali Province illustrates this upward trajectory with striking clarity[1]. In 2016, international tourist arrivals stood at 4.92 million, representing a massive 23.14% year-on-year growth rate. This momentum was maintained through 2017 with 5.69 million arrivals (15.62% growth), 2018 with 6.07 million arrivals (6.54% growth), and ultimately peaked in 2019 at 6.27 million international visitors, alongside over 10.5 million domestic tourists. During this period, the property market was largely defined by traditional hotel acquisitions and the nascent rise of the standalone private villa model, with property prices appreciating at a steady, organic rate aligned with visitor demand.

The onset of the COVID-19 pandemic in early 2020 introduced an unprecedented systemic shock to the island’s economic foundation. As global borders closed and domestic movement was restricted, international arrivals to Bali plummeted by an catastrophic 82.96% to just 1.06 million in 2020, with the vast majority of those arrivals occurring in the first quarter before comprehensive lockdowns were enforced. Domestic tourism simultaneously contracted by 56.41%. This severe demand destruction caused tourism’s contribution to the national GDP to compress from 5.0% down to 2.2%.

However, the subsequent recovery phase demonstrated the extraordinary resilience of the Bali brand. As travel restrictions eased, the island experienced an aggressive, V-shaped recovery fueled by pent-up global travel demand, the widespread adoption of remote work, and the explosive growth of the digital nomad demographic. By the end of 2024, international arrivals had strongly rebounded to 6.3 million, effectively eclipsing pre-pandemic thresholds. This resurgence catalyzed a rapid economic recovery, driving Bali’s provincial economic growth to 5.95% in the second quarter of 2025 significantly outperforming the Indonesian national average of 5.12%.

| Economic Phase | Year | Int. Arrivals (Millions) | Y-o-Y Growth | Dominant Market Characteristic |

|---|---|---|---|---|

| Pre-Pandemic Expansion | 2016 | 4.92 | +23.14% | Rapid expansion of traditional hospitality |

| Pre-Pandemic Peak | 2019 | 6.27 | +3.37% | Stabilization of hotel dominance |

| Systemic Shock | 2020 | 1.06 | -82.96% | Severe demand destruction |

| Aggressive Recovery | 2024 | 6.30 | +508% (from trough) | Speculative villa boom; oversupply inception |

| Market Recalibration | 2026 | ~6.50 (Est.) | Stabilized | Institutionalization; flight to operational quality |

The “Big Disconnect” and Market Recalibration

Despite these robust macroeconomic headline figures, a profound structural issue began to emerge beneath the surface of the real estate sector. The speculative frenzy of the recovery years (2021-2024) resulted in what industry analysts in 2026 refer to as the “Big Disconnect”. Developers, operating on the assumption of infinite linear growth in nightly rental rates, aggressively flooded the prime tourism corridors of the island with off-plan investment projects, homogenized townhouse developments, and generic short-term rental stock.

The consequence of this unchecked development pipeline is a severe, localized oversupply crisis. While overall international arrivals remain at record highs, the sheer volume of available rental listings has vastly outpaced the organic growth in the guest pool. Market intelligence derived from the management of extensive villa portfolios reveals that properties which comfortably achieved 75% occupancy rates in September 2024 experienced a precipitous decline, dropping to 35% to 40% occupancy by September 2025. This is not a transient seasonal fluctuation; it represents a fundamental structural shift in the market dynamics.

To maintain cash flow in this hyper-competitive environment, independent operators have been forced into aggressive price wars. Discounting has become the new operational standard, with property managers frequently implementing 20% to 50% rate reductions off advertised prices, increasingly relying on last-minute booking strategies that severely compress Average Daily Rates (ADR) and erode net yields. Consequently, the era of purchasing a generic “Instagram villa” in a saturated zone and expecting passive, high-margin returns is definitively over.

This cooling effect is quantitatively supported by the Bank Indonesia Residential Property Price Survey (SHPR) for the Denpasar/Bali region[2]. In the third quarter of 2025, the Residential Property Price Index (RPPI) recorded highly constrained growth of just 0.84% year-on-year, a slight moderation from the 0.90% growth seen in the second quarter. Furthermore, sales of medium and large residential units contracted significantly, with large houses seeing a massive 23% year-on-year sales decline in Q3 2025. The capital markets reflect this tightening, as 77.67% of developers are now relying on non-bank internal funds for project financing, highlighting the reduced availability of speculative commercial lending.

Simultaneously, data from Tier 1 global property consultancies confirms that institutional capital is rotating away from these fragmented, independently managed assets. Colliers International reports that global real estate fundraising rebounded by 28.9% in 2025, but capital specifically earmarked for the Asia-Pacific region surged by a remarkable 109%[3], indicating a massive structural shift in portfolio construction toward APAC markets. Within Indonesia, JLL’s 2026 outlook underscores that while the broader residential and office markets face vacancy challenges, alternative asset classes specifically data centers, lifestyle hotels, and properties located within Special Economic Zones (SEZs) are experiencing unprecedented investor demand[4].

Knight Frank’s 2026 APAC Horizon report further corroborates this trend[5], noting that in an environment characterized by slower but solid growth and elevated geopolitical risk, investors are prioritizing resilience, operational expertise, and assets capable of generating sustained income. In Bali, this translates to a massive valuation divergence between generic standard construction (averaging $355 per square meter) and luxury, professionally managed resort specifications (commanding upwards of $900 per square meter in build costs alone). Properties supported by institutional management structures, comprehensive legal compliance (such as proper NIB registration and OTA tax compliance), and integrated amenities are currently achieving 15% to 30% higher revenue and occupancy rates compared to their independent counterparts.

5 Most Profitable Districts for Investors

The maturation of the Bali property market has resulted in extreme regional fragmentation. In 2026, macro-level assumptions about “Bali real estate” are effectively meaningless; performance is entirely dictated by localized sub-market dynamics. Success requires investors to meticulously align property typologies with the specific demographic demands, saturation indices, and infrastructure pipelines of individual districts. The following analysis details the five most profitable districts for capital deployment, examining the nuanced mechanisms driving their respective valuations and yields.

This map illustrates the geographic shift in capital. While the traditional southern hubs (Seminyak, Canggu, Uluwatu) maintain high entry prices ($1,000 – $2,500/m²) and stable, single-digit growth, the new infrastructure pipeline (Toll Road) has unlocked the western frontier (Tabanan, Jembrana). These emerging areas offer significantly lower entry points ($50 – $150/m²) and massive speculative capital growth potential (28% – 40% annually). Bubble size indicates projected capital growth rate.

1. Canggu & Pererenan – Digital nomad hub, highest rental yields, starting to face limited land supply.

Canggu, alongside its immediate neighbor Pererenan, has served as the undisputed epicenter of Bali’s post-pandemic real estate boom. Having evolved from a peripheral surfing village into a dense, highly commercialized global hub for digital nomads, expatriates, and lifestyle entrepreneurs, the district commands immense global brand recognition. However, extensive market data indicates that Canggu has transitioned from a high-growth frontier into a mature, highly saturated, and stabilizing market.

The primary challenge facing investors in Canggu in 2026 is extreme inventory saturation. The district carries a “High Risk” Saturation Index of approximately 562, quantifying the intense volume of individual villas competing for a finite segment of the digital nomad demographic. This saturation has created a highly specific operational dynamic known as the “Volume Segment Paradox”. Despite representing the highest absolute volume of available units (over 354 distinct properties in the sample data), the one-bedroom villa segment in Canggu suffers from severe underperformance, recording a suppressed occupancy rate of just 63%. The density of these properties frequently leads to noise pollution, compromised privacy, and homogenous guest experiences, prompting highly mobile, price-sensitive digital nomads to continuously migrate to newer or cheaper inventory.

Conversely, multi-bedroom formats demonstrate greater resilience. The two-bedroom segment in Canggu achieves a much healthier 71% occupancy rate at a median Average Daily Rate (ADR) of $174. Yet, even in this stronger segment, growth potential is effectively zero; any attempt to implement aggressive rate hikes immediately drives consumers to the vast pool of adjacent competitors.

From a valuation perspective, land supply in prime Canggu has become acutely limited, pushing acquisition costs to the upper boundaries of the market. Premium land in the district typically lists between IDR 9 million and 14 million per square meter ($530–$825). For built assets, standard villas command $2,500 to $3,000 per square meter, while luxury and commercial resort developments exceed $3,500 per square meter.

Despite these capital constraints, Canggu remains highly profitable for investors who deploy the correct asset strategy. The district consistently delivers stabilized net annual yields between 8% and 12%. Because pure capital appreciation has largely peaked due to land price ceilings, modern investment strategies in Canggu rely on operational density and commercialization. The most lucrative assets are mixed-use commercial developments, highly integrated co-working spaces, and premium “lock-and-leave” managed apartments that offer robust acoustic insulation, high-speed fiber-optic infrastructure, and professional community management features that the standard standalone villa cannot provide.

2. Uluwatu & Bukit Peninsula – Rapid growth in the luxury resort and cliff-view villa segments.

While Canggu represents market maturation and saturation, the Bukit Peninsula specifically the corridors of Uluwatu and Bingin stands as the undisputed growth engine for luxury capital appreciation and operational yield in 2026. Characterized by dramatic limestone cliffs, white-sand beaches, and world-renowned surf breaks, the extreme topography of the peninsula naturally restricts high-density development, inherently fostering an environment of exclusivity and premium positioning.

The empirical data reveals a highly compelling arbitrage opportunity for institutional and private capital. Although Uluwatu possesses a high overall Saturation Index of approximately 647, its properties consistently capture the highest Average Daily Rates on the island. More critically, despite commanding superior nightly revenues, development-ready land in Uluwatu remains heavily undervalued relative to Canggu. Premium land in the Bukit Peninsula currently trades between IDR 5 million and 8 million per square meter ($295–$470), representing an entry cost that is roughly 40% lower than comparable plots in Canggu. This “lower entry, high ceiling” financial dynamic creates a structurally superior Return on Investment (ROI) profile.

Uluwatu dominates the high-end rental market. The two-bedroom villa segment is the absolute performance leader in the region, achieving a remarkable 72% occupancy rate alongside the highest ADR in its category at $213. Furthermore, market analysts have identified a massive supply gap in the ultra-luxury, five-bedroom estate segment. Currently, this tier faces a 50% occupancy gap due to a lack of professionally managed, institutional-grade inventory, presenting a premier opportunity for developers to introduce yield-optimized luxury assets.

Standard built villas in Uluwatu are currently valued between $1,800 and $2,200 per square meter, with the rapidly expanding luxury resort segment commanding $2,800 to $3,200 per square meter. Investors targeting the Bukit Peninsula can confidently project net annual yields between 12% and 17% the highest sustainable bandwidth currently available in the Bali market. The primary risk factors in this district are the severe logistical complexities of cliffside construction and historically constrained municipal water infrastructure. Consequently, the most sophisticated capital is bypassing independent builds and flowing directly into pre-managed luxury resort communities, where the developer has already absorbed and mitigated the foundational infrastructural risks.

3. Sanur – Stable market, benefiting from the International Health SEZ (Special Economic Zone) project.

Historically characterized as a tranquil, conservative coastal enclave favored by retirees and established expatriate families, Sanur has undergone the most radical, policy-driven structural transformation of any district in Indonesia. The singular catalyst for this evolution is the implementation of the Sanur Health Special Economic Zone (SEZ), a monumental federal initiative that has permanently altered the district’s demographic and real estate demand profile.

The Sanur Health SEZ is a 41.26-hectare enclave designed to position Bali as a world-class medical tourism destination, directly targeting the estimated IDR 86 trillion previously spent by Indonesian citizens seeking advanced healthcare abroad. Backed by a projected IDR 10.2 trillion ($620 million) in total investment, the SEZ is anchored by the fully operational Bali International Hospital (BIH) and is expected to attract up to 240,000 patients annually by 2030, while generating over 43,000 direct and indirect jobs.

From a real estate investment perspective, this macroeconomic pivot has created a highly lucrative, inelastic demand curve. The influx of elite global medical professionals, specialized wellness practitioners, administrative executives, and long-term recuperative patients requires immediate, high-quality housing. Unlike the transient, highly volatile digital nomad populations of the west coast, the demographic relocating to Sanur is forward-planning, contract-bound, and prioritizes long-term stability and proximity to the SEZ.

Consequently, Sanur boasts the lowest risk profile and the most favorable Saturation Index on the island, sitting at an extraordinarily low 53. The market is experiencing a severe structural supply deficit, particularly in the three-bedroom and four-bedroom premium family villa segments. Sanur defies its historical reputation by currently offering the highest revenue predictability in Bali. While gross nightly yields may not reach the explosive, speculative peaks of Uluwatu, the annualized occupancy stability ensures highly robust, uninterrupted net returns.

Furthermore, the stringent enforcement of the Omnibus Health Law (Law 17/2023)[6] has eradicated grey-market “wellness” clinics operating out of residential villas across other districts. By mandating hospital-grade standards and specific health facility licensing, the government has effectively granted the Sanur SEZ a localized monopoly on high-end medical and wellness tourism. Savvy investors in 2026 are capitalizing on this by developing premium, accessible, long-term lease properties specifically engineered for medical expatriates, securing steady, institutional-grade cash flow that is entirely insulated from the traditional volatility of the leisure tourism cycle.

4. Ubud – Stable in the wellness retreat and ecotourism niche market.

Nestled in the central highlands of the Gianyar Regency, Ubud operates as a vital counter-cyclical asset within the broader Bali real estate portfolio. Geographically isolated from the rapid, high-density coastal urbanization of the southern peninsula, Ubud has successfully preserved its status as the global epicenter for cultural immersion, yoga, wellness retreats, and ecotourism.

In a 2026 market defined by coastal oversupply, Ubud represents the quintessential “value” tier of premium locations. The entry barrier for built assets remains highly attractive, with standard units starting at approximately $1,060 per square meter. The market dynamics here are characterized by an exceptional degree of stability. Because the target demographic explicitly seeks tranquility, spiritual engagement, and environmental sustainability, the highly disruptive, homogenous “party villas” that have saturated Canggu are entirely obsolete in Ubud.

Investors in Ubud can project consistent, low-volatility net yields ranging between 8% and 12%. However, achieving the upper echelon of this yield bandwidth requires strict adherence to the district’s unique consumer expectations. The most successful and profitable assets in Ubud are those heavily differentiated through eco-conscious design philosophies and integrated wellness infrastructure. Properties that seamlessly incorporate smart-home climate control technologies, advanced sustainable water filtration systems, dedicated open-air yoga spaces, and the utilization of locally sourced, sustainable building materials achieve significant rental premiums.

As the Indonesian government’s 2026 infrastructure roadmap actively seeks to shift the island’s macroeconomic dependency from high-volume “mass tourism” toward high-yield “quality tourism,” Ubud is perfectly positioned to capture this affluent, ecologically aware demographic. For investors seeking a defensive asset that provides steady cash flow while avoiding the hyper-competitive price wars of the beachfront districts, Ubud remains an indispensable component of a diversified Bali property portfolio.

5. West Area (Cemagi/Seseh/Kedungu) – Natural expansion area from Canggu, land prices still undervalued with massive capital gain potential.

As the physical footprint of Canggu reaches critical mass and land acquisition costs hit their absolute ceilings, the geographical expansion of the expatriate and investment community has naturally flowed northwest along the coastline, subsuming the previously quiet agrarian villages of Seseh, Cemagi, and Kedungu. In 2026, this western coastal corridor represents the undisputed highest potential for pure, aggressive capital appreciation over the next decade.

The fundamental investment thesis for the West Area is rooted in pricing asymmetry and artificial scarcity. Land prices in this corridor remain highly attractive, averaging between $1,200 and $1,600 per square meter for standard built villas, establishing the area as a highly accessible entry point for mid-tier capital seeking beachfront proximity. However, unlike the largely unregulated, organic sprawl that characterized the early development of Canggu, municipal authorities have implemented strict spatial zoning regulations in Cemagi and Seseh.

The limited availability of designated “pink zone” land (areas legally permitted for tourism and residential development) creates a severe artificial scarcity. This regulatory framework ensures sustainable, low-density growth, effectively preserving the highly sought-after natural aesthetics unobstructed ocean views bordering traditional rice terraces that initially drew investors to Bali. This scarcity of developable plots is driving a steady, compounding appreciation in underlying land values, which have historically averaged 10% to 15% annually.

The West Area offers a highly lucrative dual-threat investment profile: investors can secure robust operational net yields of 12% to 15% via short-term rentals while simultaneously benefiting from massive long-term capital gains on the underlying land. Geographically, Seseh and Cemagi offer a serene, exclusive environment while remaining merely 15 to 20 minutes away from the dense commercial amenities, international schools, and dining infrastructure of Canggu. For investors with a medium-to-long-term horizon, securing land banks or off-plan properties in this corridor offers a highly asymmetric risk-to-reward ratio, an opportunity that is further amplified by impending, transformative infrastructure developments slated to terminate directly in this zone.

| Investment District | Primary Demographic Driver | Average Standard Build ($/m²) | Est. Net Yield (2026) | Market Phase & Capital Strategy |

|---|---|---|---|---|

| Canggu & Pererenan | Digital Nomads, Short-stay | $2,500 – $3,000 | 8% – 12% | Stabilized: High-density commercial & premium apartments. |

| Uluwatu & Bukit | Luxury Leisure, Surfers | $1,800 – $2,200 | 12% – 17% | High Growth: Luxury cliffside and ocean-view resorts. |

| Sanur (SEZ) | Medical Expats, Families | Variable (Premium Focus) | Stable/Inelastic | Structural Deficit: 3-4 BR long-term medical executive housing. |

| Ubud | Eco-tourists, Wellness | $1,060 (Entry level) | 8% – 12% | Defensive/Niche: Sustainable, green-certified wellness retreats. |

| Cemagi/Seseh | Expats, Coastal Lifestyle | $1,200 – $1,600 | 12% – 15% | Emerging Expansion: Land banking & early-stage premium villas. |

Infrastructure Projections and Their Impact on Property Prices

Global commercial real estate trends, extensively documented in reports by JLL and Knight Frank, indicate that institutional capital is overwhelmingly favoring markets where asset values are supported by definitive, state-backed structural improvements rather than mere speculative sentiment. In Bali, this macroeconomic philosophy is materializing through the deployment of multi-billion-dollar infrastructure modernization projects.

Historically, Bali’s real estate valuations have been deeply constrained by an inadequate, organic road network that failed to scale with the exponential rise in tourist and expatriate populations. For the sophisticated real estate investor in 2026, tracking these infrastructure pipelines is more critical to forecasting 10-year capital appreciation than monitoring immediate monthly tourist arrivals, as physical accessibility directly and mathematically correlates with land value appreciation. The following major infrastructure initiatives will fundamentally redefine the spatial economics of the island, redistributing capital flows and unlocking immense latent value in previously inaccessible regions.

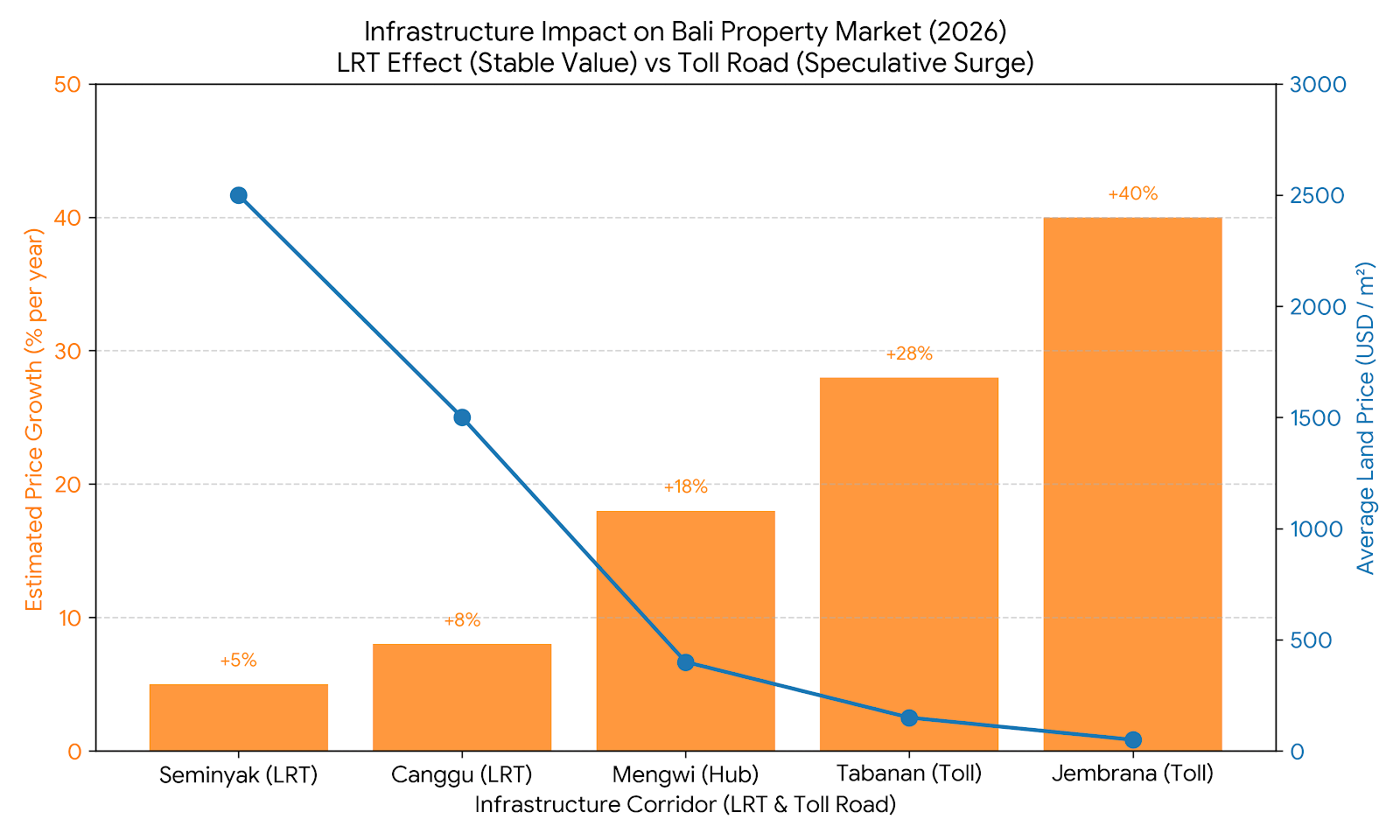

The LRT corridor (Seminyak & Canggu) has a high base price (blue line) of $1,500-$2,500/m², resulting in a moderate and stable annual growth percentage (orange bars) of 5%-8%. Conversely, the Gilimanuk-Mengwi Toll Road construction triggers massive speculation in newer areas like Tabanan and Jembrana. Although base prices are still low ($50-$150/m²), these regions lead in property investment growth percentages (+28% to +40%).

1. The Bali Urban Subway (LRT) Masterplan and the “Subway Premium”

Traffic congestion in the dense southern corridors of Bali has transitioned from a logistical inconvenience to a severe economic friction point, actively degrading the tourist experience and suppressing property values in gridlocked zones. To comprehensively resolve this crisis, the Indonesian government, in partnership with international consortia, has initiated the Bali Urban Subway, also designated as the Bali Mass Rapid Transit (MRT) or Light Rail Transit (LRT) project.

This monumental infrastructure initiative represents an estimated $20 billion total capital injection, financed entirely by the private sector on a business-to-business basis. The engineering scope is unprecedented for the island; construction officially commenced with a groundbreaking ceremony in September 2024, utilizing a fleet of ten advanced Tunnel Boring Machines (TBMs) to excavate at depths of up to 30 meters beneath Bali’s complex limestone and alluvial soil terrain.

Phase 1 of the masterplan, backed by an initial $10.8 billion investment, focuses on constructing two critical subterranean arteries designed to siphon traffic directly from the primary aviation hub:

- Line 1 (Ngurah Rai Airport to Cemagi): This 16.0-kilometer underground line will connect the international airport to Kuta Sentral Parkir, extending northward through the highly dense corridors of Seminyak and Berawa, before ultimately terminating in the emerging West Area hub of Cemagi.

- Line 2 (Ngurah Rai Airport to Nusa Dua): A 13.5-kilometer subterranean route connecting the airport southward to the luxury enclaves of Jimbaran, Unud, and Nusa Dua.

Initial commercial operations for Line 1 are aggressively targeted to commence in 2028, with the comprehensive completion of Phase 1 expected by 2031. Subsequent development (Phase 2), representing an additional $10 billion investment, will eventually extend the network eastward to Sanur and northward into the cultural heart of Ubud.

Impact on Property Prices:

The introduction of a fixed-rail, high-speed mass transit system will fundamentally and permanently

re-rate real estate valuations along its operational corridors, generating a micro-economic

phenomenon that industry analysts have termed the “Subway Premium”. As surface-level traffic remains

severely congested, the concept of “car-free tourism” is rapidly transitioning from a novelty into a

highly sought-after luxury commodity.

Properties located within a one-kilometer radius of future subterranean stations specifically in Kuta, Central Park, and the future nodes in Canggu and Cemagi are projected to experience exponential surges in market value. The LRT terminus in Cemagi acts as a particularly massive demand catalyst for the West Area. By connecting this tranquil, undervalued coastal village directly to the international airport via a high-speed underground network, Cemagi effectively bypasses the paralyzing surface traffic bottlenecks of Canggu entirely. Investors positioning capital in Cemagi and Seseh today are executing a textbook arbitrage strategy: acquiring assets at early-stage valuations while buying into a future premium transit node that will command premium rents from affluent, convenience-oriented travelers.

2. The Gilimanuk-Mengwi Toll Road: Unlocking West Bali

While the subterranean LRT project is engineered to alleviate urban density in the southern peninsula, the Gilimanuk-Mengwi toll road is designed to revolutionize interregional macro-accessibility. This surface-level highway will connect the vital industrial and ferry port of Gilimanuk on Bali’s far western tip directly to the central, urbanized hub of Mengwi in the Badung Regency.

Spanning a massive 96.84 kilometers across the Jembrana, Tabanan, and Badung regencies, the toll road carries an estimated development cost of IDR 22.8 to 24.6 trillion ($1.35 billion). The project was originally conceived to drastically compress travel times, facilitating the efficient transport of goods from the neighboring island of Java and opening the vast, undeveloped western coastline to the broader tourism economy.

However, the project’s developmental trajectory encountered significant bureaucratic friction in early 2025 when it was formally excluded from the Indonesian government’s highly coveted National Strategic Projects (PSN) list. This removal was a substantial setback, as it stripped the initiative of specific federal regulatory accelerants, expedited land acquisition powers, and direct federal investment incentives.

Despite this exclusion, the provincial government, under the directive of the Bali Governor, has firmly mandated that the toll road remains a programmed, critical development. The Ministry of Public Works has pivoted the funding strategy, transitioning the project to a model reliant on 100% private sector financing. While the loss of PSN status inherently implies that construction timelines will face extensions beyond the original 2028 operational targets as route evaluations and private tender processes are finalized, the underlying investment thesis for the region remains entirely intact.

Impact on Property Prices:

Historically, real estate values across Bali have been deeply, inversely tethered to drive times

from Ngurah Rai International Airport. By compressing the geographical distance through a high-speed

arterial route, the toll road will systematically integrate previously isolated agrarian and coastal

zones into the lucrative southern tourism matrix.

Coastal enclaves along the route, such as Medewi (a rapidly rising international surf destination), Balian Beach, and Soka Beach, stand to benefit immensely from this improved connectivity. Currently functioning as low-density, budget-friendly outposts, the eventual completion of the toll road will act as a catalyst, transforming these areas into highly viable, accessible locations for luxury eco-resorts, expansive wellness retreats, and premium residential compounds. This trajectory perfectly mirrors the developmental arc witnessed in Uluwatu a decade prior. For institutional funds, family offices, and patient private capital, the Gilimanuk-Mengwi corridor represents the ultimate long-term land-banking play, allowing acquisition at baseline agricultural prices before the infrastructure premium is priced into the market.

3. North Bali Airport and Market Decentralization

To alleviate the compounding, unsustainable strain on the southern peninsula’s infrastructure and natural resources, the provincial and federal governments are continuously advancing strategic plans for a new international airport in North Bali (Buleleng Regency). This initiative is the cornerstone of a broader macroeconomic policy aimed at decentralizing the island’s tourism economy and ensuring equitable wealth distribution across all regencies.

Supported by a $95 million government investment in supplementary infrastructure upgrades including improved arterial road networks, advanced drainage systems, and comprehensive beach restoration projects the northern coastline, specifically the Lovina corridor, is being meticulously prepared to accommodate an influx of high-yield, eco-friendly resorts and boutique villa developments.

Impact on Property Prices:

Currently, North Bali exhibits the lowest land acquisition costs on the island, primarily due to the

extensive three-to-four-hour transit time required from the southern airport. However, sophisticated

investors operating with a 10-to-15-year time horizon recognize that the establishment of a

secondary international aviation hub will instantaneously redistribute millions of tourist arrivals

directly to the north. This geopolitical shift will unlock immense latent value in Buleleng land

prices, triggering a secondary real estate boom entirely independent of the spatial and logistical

constraints currently strangling the south.

| Infrastructure Project | Scope & Investment | Estimated Timeline | Real Estate Investment Thesis & Valuation Impact |

|---|---|---|---|

| Bali Urban Subway (LRT) | $20B / 16km Phase 1 | 2028 (Phase 1 Initial) | Subway Premium: Exponential valuation surges for assets within 1km of transit nodes (Kuta to Cemagi). |

| Sanur Health SEZ | $620M / 41.26 Hectares | 2026 (Operational) | Medical Deficit: Guaranteed, inelastic demand for premium, long-term housing supporting hospital staff. |

| Gilimanuk-Mengwi Toll | IDR ~24T / 96.84km | Post-2028 (Private) | Distance Compression: Prime land banking opportunity in undervalued West Bali (Medewi/Balian). |

| North Bali Airport | New Aviation Hub | Long-term (2030+) | Decentralization: Ground-floor acquisition of coastal land in Buleleng/Lovina for future eco-resorts. |

Strategic Synthesis and Market Outlook

The empirical data defining the Bali property market in 2026 paints an unequivocal picture of an ecosystem that has fundamentally transitioned from its speculative adolescence into a highly structured, institutional-grade phase. The convergence of a rapidly tightening federal regulatory environment, a localized oversupply of generic, unmanaged assets, and the active deployment of multi-billion-dollar infrastructure networks has created a highly stratified, nuanced market that aggressively punishes operational incompetence while richly rewarding strategic foresight.

Moving forward into the next decade, the successful deployment of capital in Bali will be governed by the eradication of the speculative premium. The era in which unsophisticated investors could acquire cheap leasehold land, construct a generic villa, and reliably extract highly inflated annual yields is permanently over. Saturated hubs like Canggu will continue to heavily penalize substandard assets through plummeting occupancies and margin-crushing price wars. Value generation in 2026 and beyond is derived intrinsically from architectural differentiation, the integration of sustainable technologies, and, above all, operational excellence.

Consequently, foreign capital is overwhelmingly rotating toward Managed Resort Communities. These institutional structures shield investors from regulatory risk ensuring strict compliance with local tax frameworks and licensing mandates while leveraging economies of scale to maximize net revenue. Furthermore, over the next ten years, exponential capital gains will strictly follow the physical lines of major infrastructure developments. The Bali Urban Subway will redefine urban accessibility, while the Gilimanuk-Mengwi toll road and the North Bali Airport will systematically unlock vast, undervalued coastlines.

Simultaneously, the highest risk-adjusted returns will be increasingly found in purpose-built micro-markets experiencing structural supply deficits driven by non-tourism catalysts, exemplified by the Sanur Health SEZ. The island’s inherent global appeal, cultural resonance, and macroeconomic resilience remain entirely intact; the market simply demands a higher caliber of analytical rigor, professional management, and long-term strategic alignment to unlock its exceptional, enduring value.

References

- BPS – Statistics of Bali Province. International Tourist Arrivals to Bali by Month 2016-2026. Denpasar, Indonesia: Badan Pusat Statistik; 2026.

- Bank Indonesia. Residential Property Price Survey (SHPR) Quarter III 2025: Denpasar Region. Jakarta, Indonesia: Bank Indonesia; 2025.

- Colliers International. Global Real Estate Fundraising and Capital Flows: APAC Focus 2026. Singapore: Colliers; 2025.

- JLL. Indonesia Real Estate Investment Outlook 2026: Navigating New Asset Classes. Jakarta, Indonesia: JLL Research; 2026.

- Knight Frank. Asia-Pacific Horizon Report: 2026 Property Market Forecasts. Singapore: Knight Frank Research; 2026.

- Republic of Indonesia. Law No. 17 of 2023 concerning Health (Omnibus Health Law). Jakarta, Indonesia; 2023.